On January 15, 2026, OpenAI quietly published a document that received far less attention than it deserved. It wasn’t a product launch. It wasn’t a funding announcement. It was a Request for Proposals — a formal procurement document seeking U.S.-based manufacturers to supply hardware for OpenAI’s infrastructure over the next ten years.

Most coverage treated it as a footnote to the broader Stargate story. It is not a footnote. It is one of the most consequential industrial procurement exercises in the history of the American technology sector. The RFP is not asking for a chip supplier or a server vendor. It is asking for an entirely new domestic supply ecosystem — one capable of producing everything from precision-machined gearboxes for robotics to multi-gigawatt-capable data center cooling systems, at a scale the country has not attempted since the Cold War era of aerospace procurement.

To understand what OpenAI is actually doing here — why they structured it this way, what it demands from potential partners, how it connects to geopolitics and energy policy and consumer hardware strategy simultaneously — requires stepping back from the press release language and examining the architecture of the plan itself. This article does exactly that.

Why an RFP? The Strategic Logic Behind Going Public with Procurement

Large technology companies typically source hardware through closed procurement channels. They build relationships with a small set of approved vendors, negotiate confidential agreements, and keep their supply chain details proprietary. Apple does not issue public RFPs for iPhone components. Amazon does not broadcast its server specifications to the open market. The closed model exists for good reasons: competitive intelligence protection, pricing leverage, and operational security.

OpenAI’s decision to issue a public RFP — with a publicly listed email address, a publicly stated deadline, and a publicly described scope — is therefore a deliberate departure from standard practice. It signals several things simultaneously.

Market Development at Scale

First, it signals that OpenAI cannot satisfy its hardware needs from the existing pool of U.S.-based suppliers. The current domestic manufacturing landscape for AI-grade hardware components is simply not large enough or diverse enough to support the volumes Stargate demands. By publishing a broad, open-format RFP, OpenAI is effectively trying to catalyze a new supplier market into existence. They are telling manufacturers who currently produce components for automotive, defense, aerospace, or consumer electronics applications: there is a decade-long contract opportunity here if you can adapt your capabilities.

This is market-making behavior, not standard procurement. It is closer to what the Department of Defense does when it issues broad agency announcements for emerging technology sectors than it is to how Google buys servers.

Political and Policy Alignment

Second, the public nature of the RFP serves a political function. OpenAI is embedded in an explicit national narrative about AI leadership, reindustrialization, and economic sovereignty. Issuing a public RFP that explicitly states goals of job creation, supply chain resilience, and domestic production is not just a procurement strategy — it is a signal to policymakers, regulators, and the public that OpenAI is putting capital behind the rhetoric of American manufacturing revival.

The Stargate initiative was announced alongside the White House in January 2025. The RFP, one year later, is the operational follow-through. It tells Congress and the administration that this is real, it is happening, and here is the formal mechanism by which domestic industry will participate.

Competitive Positioning Against China

Third — and perhaps most strategically significant — the public framing of the RFP as a domestic supply chain exercise is a direct response to the geopolitical pressure around AI hardware. By documenting and broadcasting its commitment to U.S.-based manufacturing, OpenAI is building a defensible record of supply chain provenance. In an era of escalating export controls, potential tariffs, and trade decoupling, having a verifiable, auditable domestic supply chain is not just operationally prudent — it is a form of regulatory insurance.

The Three Pillars: Data Centers, Consumer Electronics, and Robotics

The RFP is organized around three distinct hardware categories, each representing a different strategic priority for OpenAI’s physical infrastructure ambitions. Understanding each category separately — and the relationships between them — is essential to grasping the full scope of what is being procured.

Category One: Data Center Hardware

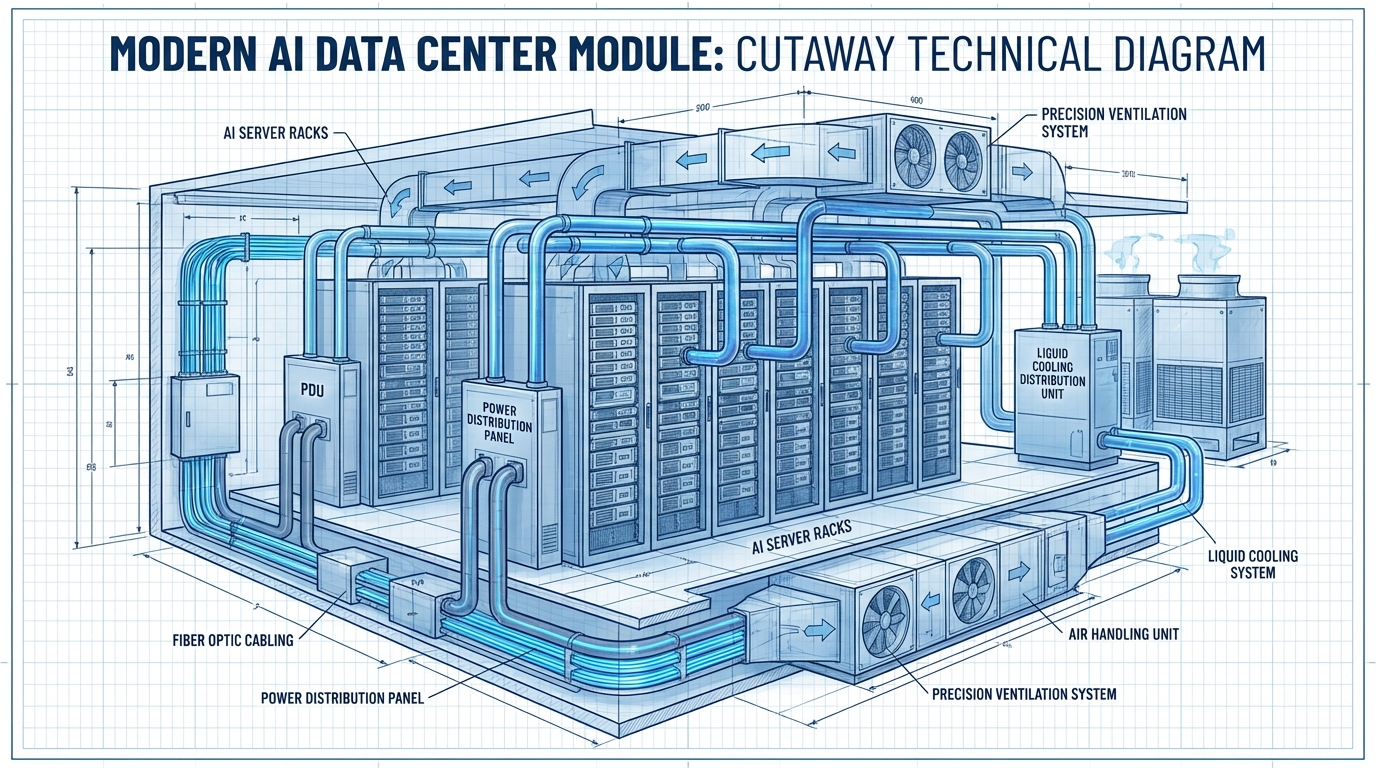

This is the largest and most immediately pressing category. OpenAI’s Stargate project requires data center infrastructure at a scale that has no real commercial precedent in the private sector. The RFP specifically targets U.S.-based manufacturers capable of supplying the physical non-chip infrastructure of a modern hyperscale AI facility: server racks, power distribution units, cabling infrastructure, networking hardware, cooling systems, and power electronics.

The cooling requirement alone is a major engineering and procurement challenge. AI compute clusters — particularly those built around high-density GPU configurations — generate heat at densities far exceeding traditional server deployments. The RFP seeks vendors capable of supplying advanced liquid cooling infrastructure, redundant thermal management systems, and the associated plumbing and fluid-handling components, all manufactured domestically.

Power electronics is another critical category. High-efficiency power conversion systems, uninterruptible power supplies (UPS) at industrial scale, busbar distribution systems, and transformer infrastructure represent a significant portion of a data center’s bill of materials — and a significant portion of what currently comes from overseas supply chains.

Category Two: Consumer Electronics

This is the category that raises the most eyebrows and the most questions. Why is an AI software company issuing an RFP for consumer electronics manufacturing capacity? The answer becomes clear when you look at OpenAI’s hardware strategy alongside the RFP. OpenAI is actively developing its first physical consumer product, expected to debut in the second half of 2026, developed in partnership with designer Jony Ive’s firm IO (acquired for $6.5 billion in July 2025). The device — widely reported to be AI-powered earbuds codenamed “Sweet Pea” — would feature a custom 2-nanometer processor and be manufactured at volumes of 40 to 50 million units in its first year.

For that kind of volume to make economic sense with a domestic manufacturing preference, OpenAI needs U.S.-based assembly capabilities, testing infrastructure, and component sourcing. The consumer electronics category in the RFP is, in part, laying the groundwork for that supply chain. The RFP seeks partners for final assembly, testing services, module production, and systems integration — the kinds of capabilities that currently exist primarily in East Asian contract manufacturers like Foxconn and Luxshare.

Whether a fully domestic consumer electronics supply chain is achievable at scale within the timeframe of an initial product launch is a legitimate question. But the RFP signals that OpenAI is at least exploring what a partially domesticated supply chain for consumer hardware would look like.

Category Three: Robotics Components

The robotics category is the most forward-looking of the three. The RFP specifically calls for domestic suppliers of gearboxes, motors, power modules, and tooling for robotic assembly lines. This category points to two parallel needs: equipping OpenAI’s own manufacturing and assembly facilities with robotics infrastructure, and building toward a future where OpenAI may be a consumer of, or participant in, the physical robotics sector.

Precision gearboxes and harmonic drives for robotics are a particular chokepoint in existing supply chains. These components — required for the smooth, precise joint movement that industrial robots need — are currently dominated by Japanese manufacturers like Harmonic Drive AG and Nabtesco. Developing U.S.-based alternatives represents both a significant engineering challenge and a significant opportunity for domestic manufacturers willing to invest in precision manufacturing capabilities.

The Stargate Connection: From Vision to Vendor Contracts

The RFP cannot be understood in isolation from Project Stargate — the $500 billion joint venture between OpenAI, SoftBank, Oracle, and MGX that was announced in January 2025 with explicit White House support.

Stargate’s stated goal is to build 10 gigawatts of AI compute capacity primarily in the United States. By early 2026, the initiative had already exceeded the halfway mark toward that 10-gigawatt commitment. The Abilene, Texas flagship facility is designed for 1.2 gigawatts of electrical capacity — a load roughly equivalent to powering 750,000 homes. A Michigan facility in Saline Township has been approved for 1.4 gigawatts. Oracle has signed agreements adding a further 4.5 gigawatts of capacity. The hardware RFP is, in effect, the procurement arm of this buildout.

The Scale of the Buildout in Practical Terms

Consider what 10 gigawatts of AI compute actually requires in terms of physical hardware. Each gigawatt of data center capacity requires thousands of server racks, tens of thousands of individual power distribution units, hundreds of miles of cabling, and cooling infrastructure capable of handling heat loads that would overwhelm conventional HVAC systems. Multiply that across multiple gigawatt-scale facilities across 16 states, and the bill of materials for just the non-chip infrastructure runs into the tens of billions of dollars.

The Stargate initiative has been projected as a $500 billion investment over four years. Even if only 20 percent of that total represents non-chip physical infrastructure — a conservative estimate — that is $100 billion in potential procurement for the kinds of manufacturers the RFP is targeting. Over a 10-year horizon with the scope of the RFP, the addressable market for domestic vendors is enormous.

Stargate as Anchor Customer

One of the most significant aspects of the RFP is the implicit promise it carries: OpenAI is positioning itself as a long-term anchor customer for whatever domestic supply chain it helps create. This matters because one of the fundamental challenges of reshoring manufacturing is the chicken-and-egg problem of investment. Manufacturers are reluctant to invest in new production capacity without guaranteed demand, and buyers are reluctant to commit to domestic suppliers who do not yet have proven capacity.

A 10-year RFP from OpenAI — backed by the financial weight of the Stargate consortium — provides the demand signal that domestic manufacturers need to justify capital investment. This is the structural insight that makes the RFP more significant than any individual product or partnership announcement.

Geopolitics as Engineering Requirement

To fully understand the urgency behind OpenAI’s manufacturing push, you need to understand the geopolitical landscape that makes a foreign-dependent supply chain a genuine strategic liability — not just a boardroom concern, but an existential risk to OpenAI’s ability to deliver on its core mission.

The Taiwan Vulnerability

The world’s most advanced semiconductor manufacturing is overwhelmingly concentrated at a single point of geopolitical vulnerability: Taiwan. TSMC, the company that manufactures the most advanced AI chips in the world including those used in NVIDIA’s data center GPUs, operates primarily from Taiwan. The geopolitical risk associated with this concentration — given the ongoing tensions between China and Taiwan — is not hypothetical. It has become a central concern in U.S. national security planning, and it is directly relevant to OpenAI’s compute strategy.

While TSMC has begun building fabrication facilities in Arizona, that capacity is years from matching the scale and capability of its Taiwan operations. In the interim, any significant disruption to Taiwan-based chip manufacturing would directly constrain OpenAI’s ability to build and operate AI systems. The hardware RFP, while not directly addressing chip fabrication, is part of a broader effort to reduce the number of single points of failure in OpenAI’s supply chain.

Export Controls and Their Second-Order Effects

U.S. export controls on advanced AI chips — particularly NVIDIA’s H100 and H200 GPUs — have created a bifurcated global market for AI compute. China and certain other nations are effectively locked out of the most powerful commercially available AI training hardware. This has generated significant pressure on the U.S. AI ecosystem in unexpected ways.

American AI companies that rely on components sourced from global supply chains face the risk of being caught between two sets of regulatory requirements: U.S. export control compliance and the sourcing dependencies that tie their hardware to countries subject to those same controls. Building a domestic supply chain for non-chip hardware components reduces one dimension of that compliance complexity.

Furthermore, as the U.S. government has signaled increasingly active interest in the AI sector — from regulatory oversight to national security reviews of foreign investment in AI infrastructure — having a predominantly domestic hardware supply chain positions OpenAI favorably in those regulatory conversations.

The “End-to-End Controllability” Principle

The RFP explicitly invokes the concept of “end-to-end controllability” in critical supply chain areas. This language is significant. It reflects a broader principle in critical infrastructure security: the idea that a system’s security is only as strong as its weakest controllable point. For AI infrastructure, end-to-end controllability means knowing not just where your chips come from, but where your power electronics come from, where your cooling systems are assembled, and where your robotic components are machined.

This level of supply chain visibility and control is not currently achievable for most technology companies operating at scale. Building it is a multi-year, multi-billion-dollar undertaking — and the RFP is the first formal step in that process.

What Vendors Actually Need to Qualify

For manufacturers considering a response to the RFP, the qualification criteria are more demanding than they might initially appear. The document is not simply asking whether a company can make the required parts. It is asking whether a company can make them at scale, reliably, and with a credible plan for expanding domestic production capacity over a decade.

Technical Capability and Speed-to-Market

The primary evaluation criterion is technical capability — specifically, the ability to meet OpenAI’s technical specifications and speed-to-market requirements. This is not just about whether a factory can produce a compliant part. It is about whether it can produce that part in the volumes, with the quality consistency, and within the delivery timelines that a multi-gigawatt data center buildout demands.

Speed-to-market is particularly critical in the data center category, where delays in component delivery can create cascade effects across an entire facility construction schedule. A vendor who can meet specs but cannot reliably deliver at volume on a tight construction timeline is not a useful partner. OpenAI’s evaluation criteria reflect this reality: proposals must include detailed timelines for scaling domestic production, not just evidence of current capability.

Factory Design and Automation Readiness

The RFP places notable emphasis on replicable factory designs and automation readiness. This signals OpenAI’s interest in manufacturing partners who have thought carefully about how to scale production without a linear increase in labor costs. A factory design that can be replicated across multiple sites is inherently more valuable to a buyer who needs to rapidly expand domestic capacity than a bespoke, one-of-a-kind production facility.

Automation readiness is similarly important. As labor costs in the United States remain significantly higher than in traditional manufacturing hubs like China and Southeast Asia, the economic viability of domestic AI hardware manufacturing depends heavily on automation. Vendors who can demonstrate high levels of robotics integration and automated quality control will have a meaningful advantage in the evaluation process.

Financial Viability and Project Delivery Track Record

The evaluation criteria also include financial viability assessments and demonstrated track records in project delivery. This is standard due diligence for any long-term procurement relationship of this scale, but it has specific implications for smaller manufacturers or newer market entrants.

A startup with a compelling technical solution but limited financial reserves and no track record of delivering large-scale manufacturing contracts will struggle to compete with established Tier 1 and Tier 2 suppliers in the evaluation process — regardless of the quality of their engineering. The RFP is, in part, structured to identify manufacturing partners who can be trusted with the execution risk of multi-year, multi-hundred-million-dollar supply agreements.

Site Characteristics and Logistical Accessibility

Proposals must also address site characteristics and logistical positioning. OpenAI is building data centers across at least 16 states. Manufacturing partners who are logistically positioned to serve multiple Stargate sites efficiently — whether through existing distribution infrastructure, strategic geographic location, or scalable logistics plans — will be more attractive than those who can only efficiently serve a single regional market.

The submission mechanism itself reflects the three-category structure: proposals are submitted via email to USMFG@openai.com with a subject line specifying the relevant category (Consumer, Robotics, or DataCenter). Proposals are accepted on a rolling basis through the June 2026 deadline, with vendor selection targeted for March 2027 and joint planning beginning in April 2027.

The Energy Equation: Power Demands That Rival Small Nations

Any serious analysis of the hardware RFP must grapple with the energy dimension of what OpenAI is building. The power requirements for Stargate-scale AI infrastructure are genuinely extraordinary — and they create both a constraint on and a driver of the domestic manufacturing strategy.

The Numbers in Context

The Stargate project targets 10 gigawatts of total AI compute capacity. To put that number in context: New York City — the largest metropolitan power market in the United States — consumes approximately 6 gigawatts of electricity at peak demand. OpenAI is building AI data centers that will collectively require more power than New York City.

Individual Stargate facilities are planned at the 1 to 1.4 gigawatt scale. The Michigan site approved in Saline Township is sized at 1.4 gigawatts — enough electricity to power over 800,000 average American homes. The Abilene, Texas flagship runs at 1.2 gigawatts, supported by dedicated West Texas wind generation and on-site power storage.

OpenAI has committed to fully funding the energy infrastructure required for each site — including dedicated power generation, transmission upgrades, battery storage, and utility partnerships — with a specific pledge that local residents will not see their electricity bills increase as a result of the data center load.

Why Energy Infrastructure Is a Manufacturing Problem

The energy dimension of Stargate is directly relevant to the hardware RFP because the equipment that manages, distributes, and conditions power at this scale — transformers, switchgear, busbar systems, UPS infrastructure, cooling integration systems — is precisely the category of hardware that the data center RFP is targeting for domestic production.

High-voltage transformer manufacturing in the United States has been a persistent bottleneck in infrastructure development. Lead times for large power transformers — the kind needed for gigawatt-scale data centers — currently run anywhere from 18 to 36 months from order to delivery, with much of that delay attributable to reliance on foreign component sourcing. Building domestic capacity to produce these components faster is not just an economic preference; it is a critical path requirement for the Stargate buildout timeline.

The Grid Modernization Opportunity

The energy requirements of OpenAI’s infrastructure buildout create what may be an unintended but significant policy opportunity: pressure to accelerate modernization of the U.S. electrical grid. Each Stargate site requires utility-level negotiations, transmission upgrades, and in many cases new generation capacity. The cumulative effect of building 10 gigawatts of private data center load across 16 states could provide the demand signal and capital investment that accelerates grid improvements that would benefit broader industrial and consumer users as well.

This is one of the more underappreciated second-order effects of the hardware RFP: by creating demand for domestic power infrastructure manufacturing, OpenAI is indirectly investing in the industrial base that the U.S. energy transition also depends on.

OpenAI’s Hardware Ambitions Beyond the Data Center

The consumer electronics category in the RFP only makes sense if you understand that OpenAI’s hardware ambitions extend well beyond building compute infrastructure. OpenAI is positioning itself to become a consumer hardware company — and the RFP is laying supply chain groundwork for that transition.

The Jony Ive Partnership and What It Signals

In July 2025, OpenAI acquired IO, the design firm founded by Jony Ive — the designer behind the original iMac, iPod, iPhone, and Apple Watch — for $6.5 billion. This was not a small talent acquisition. It was a commitment to developing physical products that could compete with the best-designed consumer hardware in the world.

Sam Altman has described OpenAI’s consumer hardware ambition in terms of creating technology that is more “peaceful and calm” than current smartphones — devices that provide deep AI integration without demanding constant visual attention. The design philosophy is one of ambient intelligence: hardware that is present and capable without being intrusive.

The device most widely reported to be OpenAI’s first physical product is codenamed “Sweet Pea” — described as AI-powered earbuds featuring a custom 2-nanometer processor capable of local AI inference, a screen-free design, and potential first-year shipment targets of 40 to 50 million units. At that scale, manufacturing strategy is a central strategic question, not an afterthought.

Why Consumer Hardware Changes the RFP Calculus

The consumer electronics dimension of the RFP introduces a fundamentally different set of manufacturing requirements compared to data center infrastructure. Data center components can be large, heavy, and built to industrial tolerances with weeks of lead time. Consumer electronics must be miniaturized, cosmetically perfect, assembled at high speed, and ready for delivery on tight seasonal schedules.

The manufacturing processes, quality control requirements, and supply chain characteristics of consumer hardware are closer to automotive or medical device manufacturing than to industrial infrastructure. Building U.S.-based consumer electronics manufacturing capacity that can compete with the efficiency of established East Asian contract manufacturers is arguably the most challenging element of the entire RFP.

However, the potential payoff is significant. If OpenAI establishes a domestic supply chain for its consumer devices and those devices achieve mass market adoption, it would represent one of the most significant demonstrations of reshored consumer electronics manufacturing since the sector largely departed the United States in the 1980s and 1990s — and a proof of concept for the broader argument that advanced consumer hardware can be manufactured competitively in the United States.

What This Means for U.S. Industrial Policy and the Reshoring Moment

OpenAI’s RFP lands at a particular historical moment in American industrial policy — one defined by the convergence of trade tension, national security concern, and bipartisan political support for domestic manufacturing investment. Understanding where the RFP fits in that larger policy landscape helps explain both its ambitions and its limitations.

The CHIPS Act Foundation

The CHIPS and Science Act of 2022 committed $52.7 billion in federal funding to semiconductor manufacturing and research, with the explicit goal of reducing U.S. dependence on foreign chip fabrication. That investment has catalyzed significant private sector commitments — TSMC’s Arizona fabs, Intel’s Ohio and Arizona expansions, Samsung’s Texas facility — but it has primarily focused on semiconductor fabrication rather than the broader hardware ecosystem.

OpenAI’s RFP extends the reshoring logic downstream from chip fabrication into the broader hardware supply chain: the racks, cooling systems, power electronics, and precision mechanical components that chips ultimately live inside. In doing so, it fills a gap that the CHIPS Act largely left unaddressed and potentially creates the kind of demand certainty that could justify additional private capital investment in domestic manufacturing capacity.

The Job Creation Dimension

The Stargate initiative has projected the creation of over 100,000 U.S. jobs directly tied to the AI infrastructure buildout. The hardware RFP, if successful in developing a robust domestic supplier base, would extend that job creation impact beyond the data center construction workforce into manufacturing, quality engineering, logistics, and supply chain management.

Manufacturing jobs in the AI hardware sector — particularly in precision mechanical components, power electronics, and advanced cooling systems — tend to be higher-skill and higher-wage than traditional assembly manufacturing. The economic multiplier effect of establishing this kind of domestic industrial base in regions that currently lack technology-sector employment is potentially significant.

Industrial Policy as Competitive Strategy

There is a broader competitive argument underlying the RFP that often goes unstated in the coverage: a nation that controls the physical manufacturing of AI infrastructure has a structural advantage in AI capability that cannot be easily matched by a nation that is dependent on foreign supply chains for the same infrastructure.

This is not a new insight — it is the same logic that has driven military procurement policies for decades. But it is being applied here to commercial technology infrastructure in a way that represents a meaningful expansion of how “strategic industries” are defined in U.S. industrial policy. OpenAI’s RFP is, in part, an argument that AI compute infrastructure should be treated with the same supply chain sovereignty concerns as defense manufacturing — and that private sector investment can lead that effort without waiting for government mandates.

The Timeline Reality Check

The RFP’s stated timeline is precise, but the gap between a timeline in a procurement document and the actual delivery of new domestic manufacturing capacity is substantial. A clear-eyed assessment of what is realistically achievable — and by when — is essential for anyone trying to understand what the RFP will actually accomplish.

The Formal Timeline

The key dates in the RFP process are: proposals accepted on a rolling basis through June 2026; vendor selection completed in March 2027; joint planning and partnership kick-off in April 2027. From there, actual production ramp-up would depend on the specific vendor and category, but the 10-year horizon of the RFP suggests that OpenAI expects the full domestic supply chain buildout to take until roughly 2036 to complete.

The Capacity-Building Gap

Building new manufacturing capacity in the United States takes time — often more time than technology roadmaps allow for. Environmental permitting, facility construction, equipment procurement, workforce training, and quality certification processes all take years, not months. A vendor who receives a contract award in March 2027 will not be producing at scale for at least 18 to 24 months after that — potentially pushing meaningful domestic production into 2029 or 2030.

For the most technically demanding categories — precision gearboxes for robotics, high-efficiency power electronics, advanced cooling systems — the ramp-up timeline may be even longer, as these require specialized manufacturing equipment and skilled workforce development that do not exist in significant quantities in the current U.S. manufacturing base.

The Rolling Stargate Demand

The saving grace for the timeline concern is that the Stargate buildout is itself a multi-year, rolling program. OpenAI is not building all 10 gigawatts simultaneously. Facilities are being planned, permitted, and constructed across different states on staggered timelines. This means that domestic vendors who come online in 2029 or 2030 can still capture a significant portion of the total Stargate procurement opportunity, even if the earliest sites are built primarily with components from existing supply chains.

The phased nature of Stargate also gives domestic manufacturers a more forgiving demand curve to grow into — which is precisely why OpenAI structured the RFP as a 10-year instrument rather than a 2-year spot contract.

Risks, Unknowns, and Legitimate Questions

No analysis of the RFP would be complete without addressing the genuine risks and uncertainties that surround it. The plan is ambitious, but ambition is not a guarantee of execution.

Cost Competitiveness of Domestic Manufacturing

The fundamental economic challenge of reshoring manufacturing is cost. Labor costs in the United States are 5 to 10 times higher than in China for comparable manufacturing roles. Even with aggressive automation, domestic production of hardware components will carry a cost premium relative to equivalent production in established Asian manufacturing hubs. OpenAI’s willingness to absorb that premium — and the degree to which it can drive automation investment to close the gap — will determine whether the domestic supply chain it builds is economically durable or structurally dependent on the patronage of a single anchor customer.

Workforce Availability

The U.S. manufacturing workforce has contracted significantly over the past three decades. The skills required for precision mechanical manufacturing, power electronics assembly, and advanced cooling system production are not widely available in the current labor market. Building the workforce pipeline — through community college programs, apprenticeships, and employer training investments — takes years and requires coordination between private sector employers and public educational institutions that is notoriously difficult to achieve at scale.

Supply Chain Depth vs. Final Assembly

There is a risk that the domestic supply chain OpenAI builds is shallow rather than deep — meaning that final assembly may occur in the United States, but the sub-components and raw materials used in that assembly continue to come from overseas. A data center rack assembled in Texas from Chinese-sourced steel, Taiwanese-sourced power electronics, and South Korean-sourced cooling components is “domestically manufactured” in a legal and procurement sense but does not address the supply chain resilience concerns that motivate the RFP in the first place.

Ensuring genuine depth in the domestic supply chain — meaning that multiple tiers of component production are localized, not just final assembly — requires a level of supplier development investment and coordination that goes significantly beyond what a single procurement document can achieve.

What Happens If Stargate Slows Down

The demand signal that makes the hardware RFP credible is the Stargate buildout. If that buildout slows — due to capital constraints, regulatory challenges, changes in AI demand forecasts, or shifts in OpenAI’s competitive position — the demand certainty that underpins vendor investment decisions disappears. Manufacturers who have made capital commitments based on the RFP’s implied demand would face significant financial exposure.

This is not a hypothetical risk. Large infrastructure programs with private capital at their core have a history of revisions, delays, and scope changes. The 10-year horizon of the RFP provides some buffer, but it does not eliminate the execution risk that comes with betting on a single buyer’s long-term demand projections.

The Physical Foundation of AI Supremacy: What the RFP Tells Us About OpenAI’s World View

Step back from the procurement details and the geopolitical context, and the hardware RFP reveals something fundamental about how OpenAI’s leadership thinks about the nature of AI competition and the requirements for long-term leadership in the field.

There is a school of thought in the AI industry that hardware is a commodity — that the real competition happens at the model, algorithm, and product layer, and that hardware infrastructure is best sourced from whoever can provide it most efficiently, regardless of geography. OpenAI’s RFP is a direct repudiation of that view.

The RFP reflects a belief that in the long run, the ability to build and control the physical infrastructure on which AI systems run is itself a form of competitive advantage — and that an AI company that depends on foreign supply chains for its physical foundation is structurally vulnerable in ways that no amount of algorithmic sophistication can fully compensate for.

This is a significant strategic claim. If OpenAI is right, then the companies and nations that invest now in domestic AI hardware manufacturing will have structural advantages a decade from now that will be very difficult for latecomers to close. If they are wrong — if hardware remains a commodity and domestic manufacturing proves uncompetitively expensive — then the RFP will represent a costly strategic miscalculation.

The honest answer is that no one knows yet which view will prove correct. But the willingness to make a 10-year, multi-billion-dollar bet on the physical dimension of AI competition tells you more about OpenAI’s strategic confidence — and its read of the geopolitical environment — than almost any other decision the company has made in 2026.

Conclusion: What to Watch For — and What It Means If It Works

The OpenAI hardware RFP is a long game. Its full implications will not be visible for years. But there are specific signals to watch that will indicate whether the initiative is delivering on its ambitions or running into the structural obstacles that have frustrated previous reshoring efforts.

Watch the vendor selection announcements in March 2027. The identity and scale of the companies chosen — whether they are established Tier 1 manufacturers pivoting to AI hardware, or new entrants purpose-built for this opportunity — will tell you a great deal about whether a genuine domestic supplier base is materializing or whether the RFP is being satisfied primarily by existing contractors with thin domestic manufacturing footprints.

Watch the first Stargate facilities that come online after 2027. The extent to which their supply chains are genuinely domestic — measured in component origin, not just final assembly location — will be the real test of whether the RFP is building supply chain depth or supply chain theater.

Watch the consumer hardware launch. If OpenAI’s first consumer device achieves meaningful domestic manufacturing content at 40 to 50 million units per year, it will be one of the most significant demonstrations of reshored consumer electronics manufacturing since the sector largely departed the United States in the 1980s and 1990s.

Watch the energy infrastructure. The power systems and cooling hardware required for Stargate’s gigawatt-scale facilities will be among the first major categories where domestic manufacturing either proves its capability or reveals its limitations. This is where the rubber meets the road for the RFP’s most immediately critical procurement needs.

If the RFP succeeds at even a fraction of its stated ambition — if it catalyzes a genuine expansion of U.S. manufacturing capacity in AI hardware, creates the industrial jobs it promises, and reduces OpenAI’s dependency on geopolitically exposed supply chains — it will stand as one of the more consequential industrial policy initiatives of the decade. Not because of the technology it produces, but because of the physical infrastructure it builds beneath it.

AI runs on software. But software runs on hardware. And hardware, it turns out, runs on industrial policy, supply chain strategy, and the willingness to make very long bets on very physical things. OpenAI’s 10-year hardware RFP is exactly that kind of bet.