For most of fintech’s history, the question at the center of every product decision has been the same: what does the human want? Payment flows, KYC frameworks, API rate limits, spending controls — all of it was engineered around a human at one end of the transaction, even when that human was buried five layers deep inside an automated workflow.

That assumption is cracking. Not theoretically — in production, right now, in 2026.

Coinbase’s “Coinbase for Agents” infrastructure, built on top of the CDP (Coinbase Developer Platform) AgentKit, has done something more structurally significant than launching another crypto product. It has begun treating the AI agent as the primary financial actor — an entity that holds a wallet, initiates payments, executes trades, subscribes to data services, and settles obligations with stablecoins, all without a human clicking “confirm.”

This is not the same conversation as “AI in fintech.” Robo-advisors, fraud detection models, and underwriting algorithms have used AI inside fintech systems for years. What Coinbase for Agents represents is different: giving the AI itself financial agency. The model doesn’t just recommend — it transacts.

The implications for anyone building or operating fintech infrastructure in 2026 are difficult to overstate. But so are the gaps, the risks, and the parts of the story that aren’t making it into the press releases. This article covers all of them — the actual architecture, the real use cases, the meaningful differences from traditional fintech automation, and the compliance questions that will define whether this technology scales or stalls.

What “Coinbase for Agents” Actually Is — And What the Headlines Miss

The phrase “Coinbase for Agents” has been used loosely enough that it’s worth pinning down precisely. It refers to a suite of Coinbase Developer Platform (CDP) products designed specifically for AI agents as the primary user type — not a human-facing product that agents can optionally access, but infrastructure architected from the ground up around non-human financial actors.

The core components are:

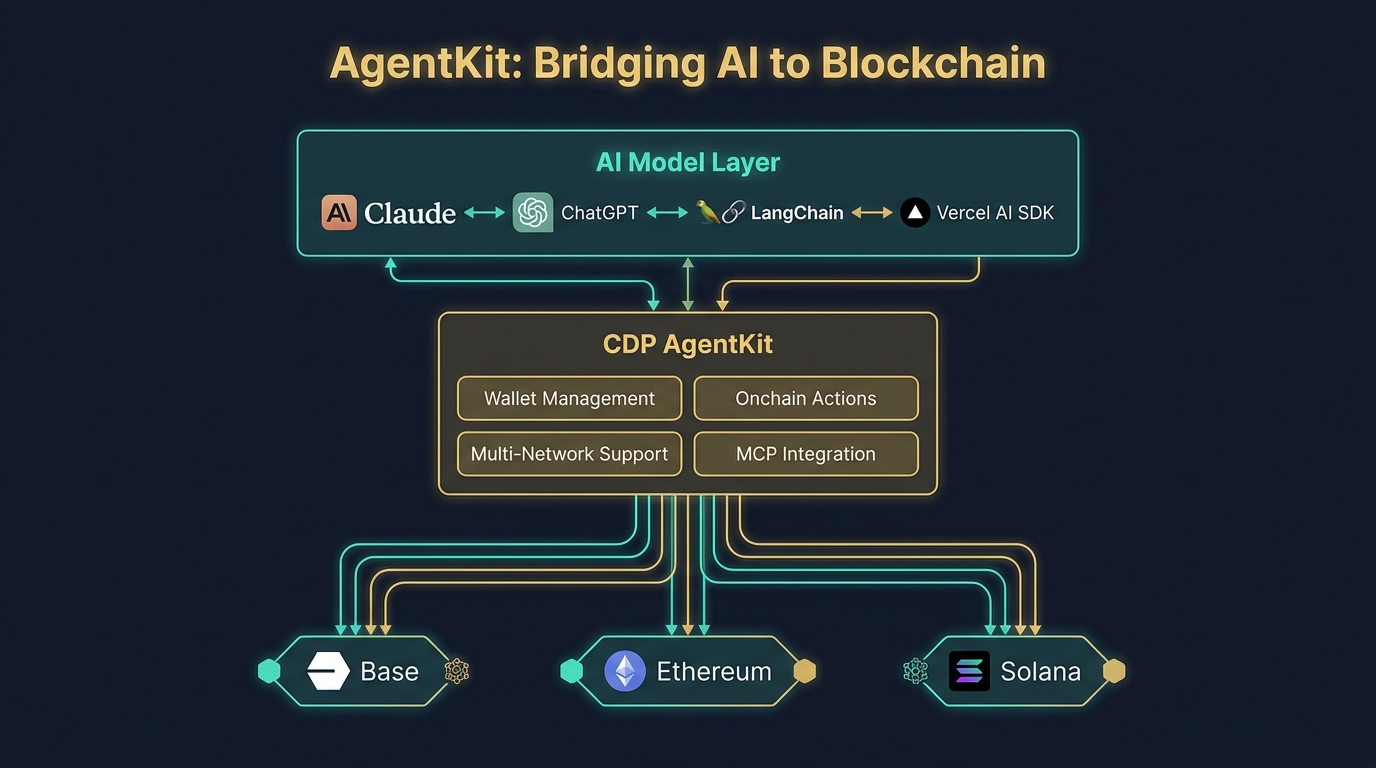

- CDP AgentKit — The developer SDK that gives AI agents secure wallet management and onchain action capabilities. AgentKit is model-agnostic (works with LangChain, Eliza, Vercel AI SDK, and others), framework-flexible, and supports EVM-compatible networks plus Solana.

- Agentic Wallets — Programmable crypto wallets purpose-built for non-human actors, with configurable spending limits, policy-based controls, and multi-network support across Base, Ethereum, and Solana.

- x402 Payment Protocol — An HTTP-native stablecoin micropayment standard built on the long-dormant HTTP 402 “Payment Required” status code, enabling instant pay-per-request transactions between agents and APIs.

- MCP Integration — Native compatibility with Anthropic’s Model Context Protocol (MCP), allowing Claude, ChatGPT, and other models to connect to CDP tooling as external actions within their agent stacks.

- Agentic Trading — A consumer-facing product launched in 2026 that allows AI agents connected to Coinbase accounts to autonomously execute crypto trades and pay for premium market data on behalf of users.

What the headlines tend to flatten is the distinction between these layers. Some coverage treats AgentKit as the whole story. Others focus on Agentic Trading as a consumer curiosity. The more consequential angle — and the one relevant to enterprise and developer teams — is how these components compose into a full financial automation stack for software agents that previously had no native way to hold or move money.

The Shift from API Access to Financial Agency

Traditional fintech APIs let software systems query balances, initiate transfers, and read transaction histories — but always on behalf of a verified human account holder. The software is the messenger; the human is the principal. Coinbase for Agents inverts this by making the agent itself the account holder. It can own assets, execute value transfers, pay for services it needs, and settle obligations with counterparties — all without routing every action through a human-owned account.

That architectural distinction matters enormously for what kinds of automation become possible. An AI agent that needs to pay a data API for each query, tip a content creator for a used asset, or split a payment across multiple counterparts after completing a task — none of that works smoothly on traditional banking rails. All of it is native to the Coinbase for Agents stack.

AgentKit: The Technical Layer That Makes It Work

AgentKit is the foundational SDK sitting underneath everything else. Built on the Coinbase Developer Platform SDK, it provides four core capabilities that collectively answer the question: how does an AI agent actually interact with financial infrastructure?

Secure Wallet Management

AgentKit allows AI agents to create and manage crypto wallets without requiring a human account to serve as the parent entity. Each agent wallet is isolated, with its own keys managed through CDP’s infrastructure. The critical design choice here is that wallet creation is programmatic — an orchestration system can spin up purpose-specific wallets for individual agent tasks and tear them down afterward, rather than using a single shared wallet that creates both security and accounting headaches.

This matters practically. A research agent that needs to pay per API call, a trading agent managing a portfolio, and a yield agent seeking DeFi returns can each operate from separate wallets with separate spending limits and separate audit trails. The financial footprint of each agent task is cleanly separable — which is the prerequisite for any serious internal governance model.

Onchain Action Library

AgentKit ships with a library of predefined onchain actions: token transfers, swaps, smart contract deployments, NFT interactions, DeFi protocol integrations, and custom contract calls. These actions are exposed as callable tools that any connected AI framework can use. When a LangChain agent or a Claude MCP server requests an onchain action, AgentKit handles the transaction construction, gas estimation, signing, and broadcast — abstracting the blockchain complexity entirely away from the agent logic above it.

The extensibility here is significant. Teams can add custom actions by extending the base toolkit, which means proprietary DeFi integrations, company-specific smart contract interactions, or industry-specific financial primitives can be wrapped and made available as first-class agent capabilities alongside the out-of-box ones.

Multi-Network and Framework Agnosticism

AgentKit’s deliberate neutrality on both the model side and the network side reflects a considered design philosophy. On the AI side, the toolkit doesn’t care whether the agent is powered by Claude, GPT-4o, Gemini, or an open-source model — it exposes a standard interface that any framework can consume. On the blockchain side, it supports any EVM-compatible network plus Solana, which in practice means Base (Coinbase’s own L2), Ethereum mainnet, and the growing ecosystem of EVM chains.

The Base network preference isn’t just branding. Base offers transaction finality in roughly two seconds and fees typically measured in fractions of a cent — both of which matter materially for the kind of high-frequency, low-value transactions that characterize agent micropayment patterns.

MCP Connectivity

The integration with Anthropic’s Model Context Protocol is where AgentKit connects to the broader ecosystem of AI tooling. With MCP, Claude-based agents can treat CDP capabilities as externally-accessed tools — meaning a Claude agent can trigger an onchain payment, check a wallet balance, or execute a swap through the same tool-calling interface it uses for web search or code execution. More than 10,000 public MCP servers are now active in the ecosystem, and 75+ Claude connectors have been built on the protocol, which makes MCP compatibility a serious distribution lever for any infrastructure provider.

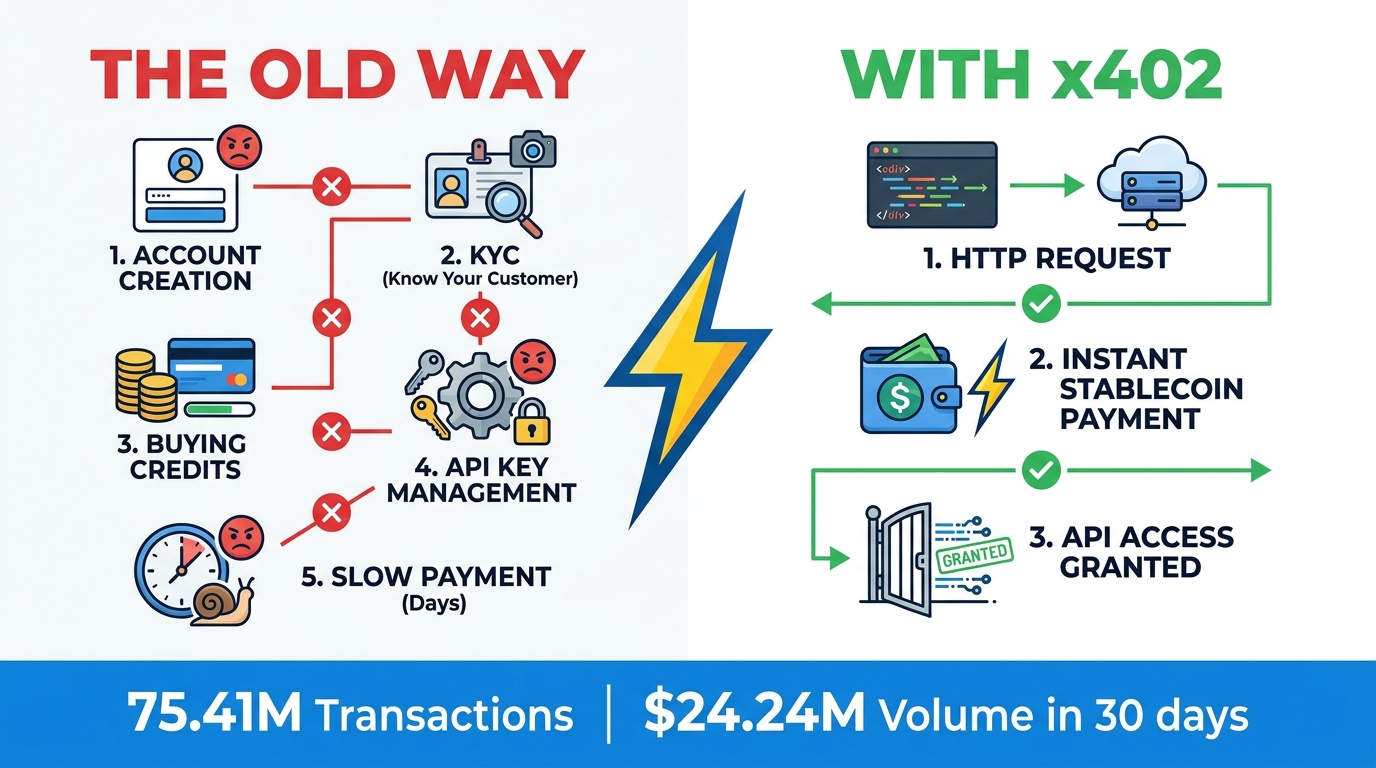

x402: The Protocol That Wants to Replace API Keys

The HTTP status code 402 has technically existed since 1991. It was defined in the original HTTP specification as “Payment Required” and was immediately reserved for future use — future use that never arrived, because the internet had no native mechanism for machines to actually pay for things programmatically. That reserved status code sat dormant for over three decades.

x402 finally activates it.

How the Protocol Actually Works

The flow is architecturally simple, which is precisely why it’s significant. An AI agent makes an HTTP request to a resource or API. If payment is required, the server returns a 402 status code along with a payment manifest detailing the price, accepted currencies, and supported blockchain networks. The client — which in this context is the AI agent’s wallet infrastructure — reads the manifest, executes the stablecoin payment onchain, and retries the original request with a payment proof header. The server verifies the proof and grants access.

The entire cycle happens in seconds. No account creation. No KYC. No API key provisioning. No subscription management. No waiting for a billing cycle. The agent pays for exactly what it uses, precisely when it uses it, and the payment is settled on-chain with cryptographic proof attached to every request.

The Numbers Behind Early Adoption

x402 has crossed thresholds that move it from prototype to measurable infrastructure. In a recent 30-day window, the protocol processed 75.41 million transactions with $24.24 million in volume across approximately 94,000 buyers and 22,000 sellers. Those figures tell a specific story: the transaction count vastly exceeds what you’d expect from human-initiated micropayments. The volume is being driven by agent-scale request patterns — high frequency, low individual value, continuous operation.

What’s particularly notable is the buyer-to-seller ratio. Roughly four buyers per seller suggests a market structure where a relatively small number of API providers and data sources are being accessed by a much larger, rapidly growing population of agents. That ratio will likely invert or flatten as more sellers integrate the protocol, but the early shape indicates real demand-side pull.

x402 vs. Traditional API Monetization

The traditional API economy runs on a model that was designed for human developers: create an account, submit to terms of service, add a payment method, purchase a subscription tier or credit bundle, receive an API key, rotate that key periodically for security, and manage billing at the end of each cycle. Every step in that process assumes a human making deliberate decisions.

For an AI agent operating autonomously — discovering APIs dynamically, needing to pay per request based on actual usage, potentially interacting with thousands of different services — that model creates enormous friction. x402 collapses that friction to a single atomic transaction that happens inline with the request itself. The agent’s wallet pays; the API serves. No human has to provision credentials, manage subscriptions, or reconcile billing in between.

This is not a marginal improvement. It’s a different category of interaction that makes whole classes of agent behavior economically viable that previously weren’t — including real-time data access, specialized compute purchases, and agent-to-agent service markets.

The USDC-First Architecture: Why Stablecoins, Why Now

Every component of the Coinbase for Agents stack settles primarily in USDC — Coinbase’s co-issued US dollar stablecoin — with execution typically happening on the Base L2 network. This is not the only technically possible design, but it’s a deliberate strategic choice with real operational logic behind it.

Why Not Volatile Crypto

An AI agent making autonomous payments cannot dynamically adjust its behavior to account for an asset that might be worth 30% less by the time a transaction settles. The moment you introduce price volatility into a programmatic payment flow, you create a class of problems — miscalculated budgets, unexpected losses, broken accounting logic — that defeat much of the purpose of automation. USDC’s peg to the US dollar eliminates this variable. The agent that approves a $0.003 per-request payment is paying $0.003, not $0.003 ± market conditions.

Why Not Traditional Fiat

The alternative — routing autonomous agent payments through traditional fiat rails — runs into a different set of problems. ACH transfers settle in one to three business days and require the originating account to be linked to a verified banking relationship. Wire transfers are faster but expensive and still require human-associated accounts. Card transactions involve interchange fees, chargeback risk, and card network rules that weren’t written with autonomous software actors in mind.

USDC on Base settles in approximately two seconds with fees often below one cent. For micropayments at agent scale — potentially millions of transactions per day — the economics of traditional fiat rails are simply not viable.

Programmable Spending Controls

One of the quieter but more important features of the Agentic Wallet infrastructure is the ability to define programmable spending policies. Rather than giving an agent unrestricted access to a wallet, operators can configure per-transaction limits, daily caps, allowlisted counterparty addresses, and approval requirements for transactions above certain thresholds.

This is the feature that bridges the gap between what autonomous agents can theoretically do and what enterprise risk management will actually allow in production. An agent with an uncapped, unconstrained wallet is an obvious liability. An agent with a $50 daily spend limit that can only transact with pre-approved counterparties is a much more manageable operational unit — even if it’s still fundamentally autonomous.

Real-World Use Cases Already Running in 2026

Beyond the architectural framing, a set of concrete use patterns has emerged in the market. Some are developer-scale experiments; others are at production volume. Understanding which is which matters for teams evaluating where to invest attention.

Pay-Per-Request Data and Compute Access

The most mature use case is agent-driven API payments via x402. Research agents, trading agents, and data analysis pipelines are using the protocol to access premium data sources on a per-query basis — paying for satellite imagery, financial data feeds, market microstructure data, and AI inference endpoints without pre-purchasing subscription access. The economic advantage is real: agents pay only for what they use, and data providers receive payment atomically rather than managing billing relationships.

Gaming and Digital Asset Economies

The clearest production-scale case study in the Coinbase ecosystem is Blocklords Dynasty, a web3 game using CDP’s Paymaster to enable gasless onboarding. The numbers are publicly available: 1.2 million-plus wallets supported, 50 million-plus in-game transactions, and 250,000-plus daily active users — all without requiring players to manually manage wallet operations. This case demonstrates something important: agent-style wallet infrastructure works at scale when the complexity is appropriately abstracted away from the end user.

FereAI and Autonomous Trading Research

FereAI, highlighted in Coinbase’s developer case study materials, demonstrates the agentic trading research pattern: an AI agent that monitors market conditions, accesses premium data (paying via stablecoin micropayments), performs analysis, and executes trades within configured parameters — all autonomously. The agent acquires what it needs to operate as it needs it, rather than requiring a human to pre-provision all its resources.

Autonomous Treasury Management

An emerging enterprise pattern is treasury agents that autonomously manage onchain liquidity — moving idle balances into yield-generating DeFi positions, rebalancing allocations based on rate changes, and executing internal transfers between business units. These agents operate within pre-approved policy parameters and generate complete audit trails through the immutability of onchain records. The appeal for finance teams is obvious: yield optimization that runs continuously without requiring round-the-clock human oversight.

Agent-to-Agent Service Markets

The most forward-looking pattern is one where AI agents sell services to other AI agents — a research agent contracting a computation agent for processing power, or a data-cleaning agent billing a downstream pipeline agent for its output. x402 makes this technically feasible with no intermediary infrastructure required. Whether this pattern reaches meaningful scale in 2026 or 2027 remains to be seen, but the protocol-level groundwork is in place.

How Coinbase for Agents Differs from Traditional Fintech Automation APIs

There’s a temptation to frame Coinbase for Agents as the next evolution of traditional fintech automation APIs — as though Plaid, Stripe Treasury, or banking-as-a-service platforms are simply being superseded. That framing gets it wrong. These are different tools designed for different problems, and understanding the distinction is essential for making intelligent build-vs-integrate decisions.

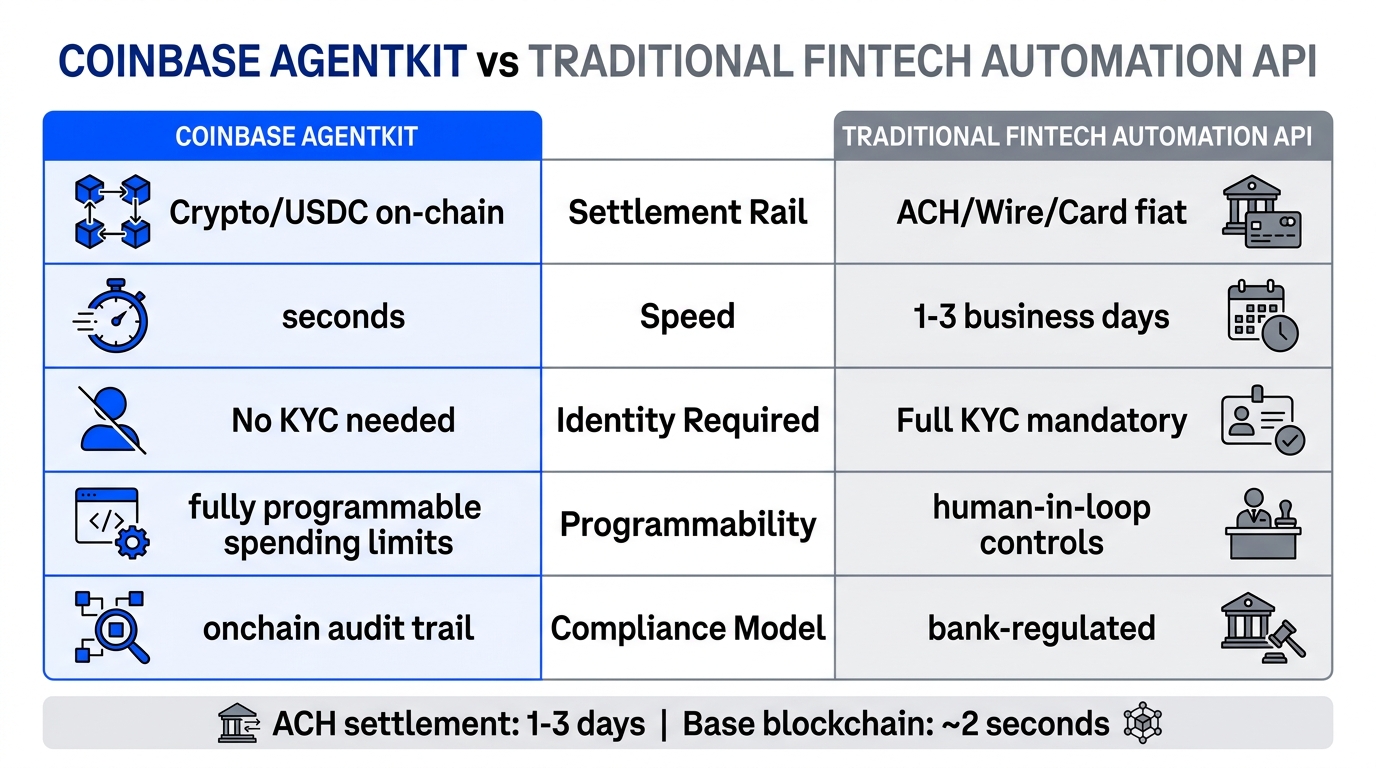

The Rail Difference

Traditional fintech automation APIs — whether from Plaid, Stripe, Marqeta, or direct bank API programs — operate on fiat rails: ACH, wire transfer, card networks, and emerging real-time payment systems like RTP and FedNow. These rails are deeply integrated with the regulated banking system, which means they carry both the protections and the constraints of that system: FDIC insurance, Regulation E consumer protections, established chargebacks, and institutional counterparty trust.

Coinbase for Agents operates primarily on crypto rails — Base blockchain, Ethereum, Solana — settled in USDC. The assets are not FDIC-insured. There are no chargebacks. The transaction finality is cryptographic rather than institutional. These aren’t necessarily disadvantages, but they are fundamentally different risk and trust characteristics that any responsible deployment needs to account for.

The Identity Difference

Every traditional fintech API assumes a verified identity at some layer of the stack. Plaid links to a real bank account belonging to a real, KYC’d person. Stripe processes payments on behalf of a registered business. Even banking-as-a-service platforms that abstract the bank relationship still require identity verification at onboarding.

Coinbase for Agents — particularly through x402 — explicitly removes the identity requirement for transacting. An agent can pay for and receive API access with no account creation, no identity documents, and no human name attached to the transaction. This is enormously useful for agent scalability and removes significant operational friction. It also creates a meaningful accountability gap that has regulatory implications discussed in the next section.

The Programmability Difference

Traditional fintech automation allows programmability within defined parameters set by banking partners and card networks. You can automate transfers, trigger conditional payments, and build rules-based workflows — but the programmability ceiling is set by the banking institution or payment network’s API contract, not by what you technically want to do.

AgentKit allows substantially deeper programmability: arbitrary smart contract interactions, custom DeFi strategy execution, agent-defined payment splits, and new token mechanics that have no analog in the traditional payments world. The ceiling is much higher. So is the surface area for things going wrong in novel ways.

Where They Complement Rather Than Compete

The most pragmatic framing is that these two approaches handle different parts of the automation stack well. Traditional fintech APIs remain the right tool for fiat-denominated transactions, regulated financial products, consumer-facing banking experiences, and any workflow that requires the trust infrastructure of the traditional banking system. Coinbase for Agents is the right tool for crypto-native value transfer, agent-to-agent micropayments, programmable onchain treasury management, and any workflow where the agent itself needs to be the financial principal rather than a proxy for a human account.

Many real-world deployments in 2026 will use both — a traditional banking API for fiat settlement with counterparties, and AgentKit for the internal agent economy that manages and moves the crypto-denominated portion of a treasury or operational budget.

The Multi-Agent Stack: Orchestration, Delegation, and DeFi

Single-agent deployments are the entry point, but the architectural direction clearly points toward multi-agent systems — hierarchical networks of specialized agents where financial authority is delegated, not concentrated.

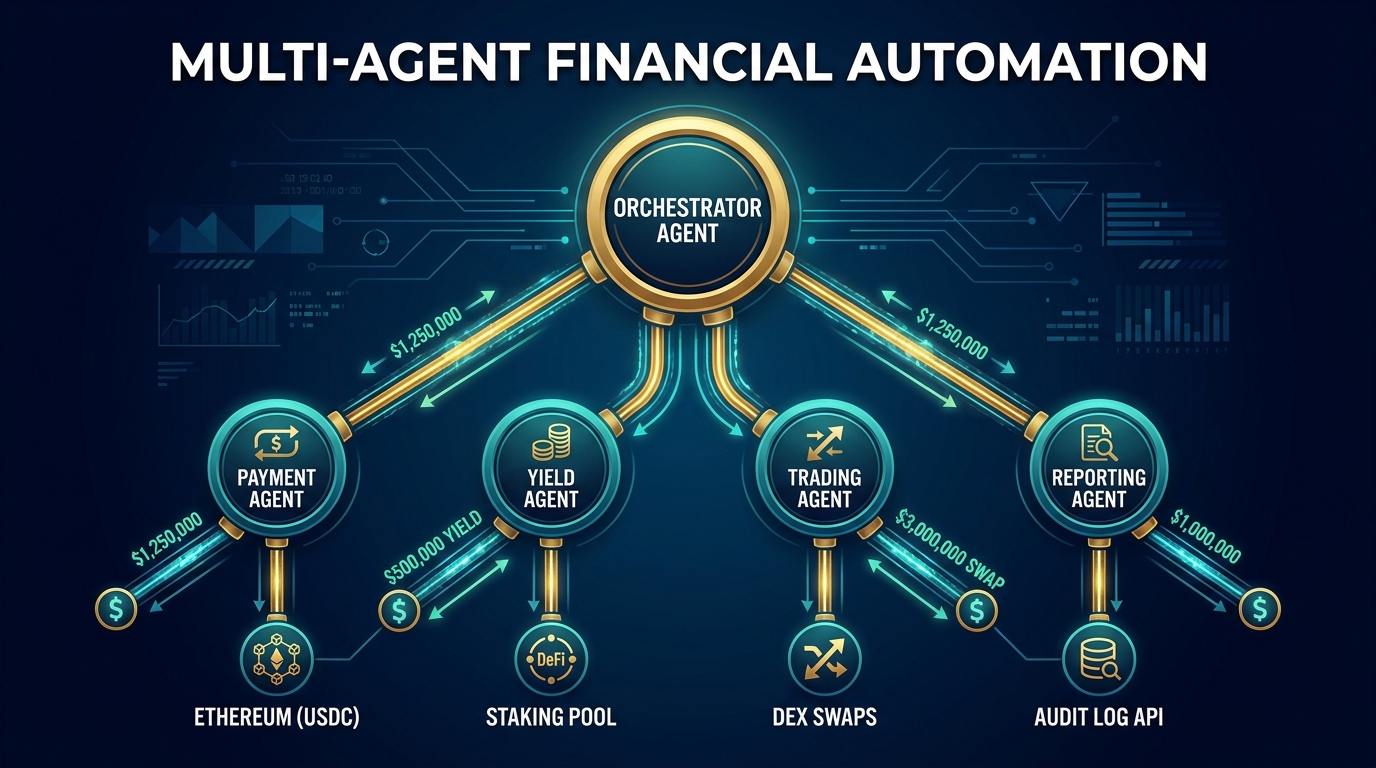

The Orchestrator-Executor Model

The pattern that’s emerging in more sophisticated deployments looks like this: an orchestrator agent at the top of the hierarchy receives a high-level objective (optimize treasury yield while maintaining $X in liquid reserves), breaks it into sub-tasks, and delegates those sub-tasks to specialized executor agents, each of which has its own wallet with spending limits appropriate to its function.

A payment executor handles disbursements to vendors and counterparties. A yield executor manages DeFi positions. A trading executor handles market operations within a risk-bounded policy. A reporting executor writes audit records and generates human-readable summaries for oversight review. None of these agents can operate outside their defined scope — the programmable wallet policies enforce that constraint at the infrastructure level, not just in application code.

This architecture matters because it mirrors the way enterprise finance teams already think about role separation and controls. A treasury analyst doesn’t have the same authorization as a CFO. The same principle applies to agent hierarchies, and AgentKit’s programmable wallet policies make it technically enforceable rather than just a policy document.

DeFi Integration: Yield and Liquidity Automation

One of the more practically significant use cases emerging from the multi-agent pattern is automated DeFi yield management for corporate treasuries. Enterprises with crypto-denominated reserves — or those choosing to hold stablecoin working capital — can deploy agents that continuously seek yield across approved DeFi protocols, adjusting positions based on rate changes, liquidity depth, and counterparty risk scores.

This is not theoretical. The DeFi yield automation pattern is already visible in sophisticated crypto-native organizations and is migrating toward more traditional enterprise contexts as the tooling matures. The key difference from human-managed DeFi positions is continuous operation: an agent doesn’t sleep, doesn’t take weekends off, and doesn’t miss a yield opportunity because someone was in a meeting. The value proposition is the same as any treasury automation, amplified by the 24/7 nature of onchain markets.

Agent-to-Agent Delegation and Trust

Multi-agent systems introduce a new class of trust question that doesn’t exist in single-agent deployments: when Agent A delegates a financial task to Agent B, how does the infrastructure verify that Agent B’s actions are actually within the scope of that delegation, and not a compromised or misbehaving agent acting outside its authority?

This is an active area of development in the CDP ecosystem. Onchain delegation records — where the authorization scope of each agent is written to the blockchain as an immutable artifact — represent one architectural answer. Spending policy enforcement at the wallet level, independent of the agent’s own code, represents another layer of protection. But the full trust architecture for complex multi-agent financial systems is still being worked out in the field.

The Compliance and Risk Problem Nobody Is Talking About Loudly Enough

Every honest analysis of Coinbase for Agents has to spend serious time here, because the compliance and risk profile of autonomous agent payments is genuinely unresolved — and the people who will be most affected are the enterprises and developers building on top of this infrastructure, not the infrastructure providers themselves.

The Accountability Gap

Traditional financial regulation is built on a foundational assumption: there is always a human legal entity responsible for every financial transaction. The KYC/AML framework exists to verify who that entity is and to ensure they’re not on a sanctions list. When an AI agent transacts autonomously, with no human identity attached to the transaction at the point of execution, the accountability question becomes genuinely unclear.

Coinbase’s position is that the human or business that configures and deploys the agent is the legally responsible party, and that the programmable spending limits and pre-approved counterparty lists represent the controls that make this manageable. That’s a reasonable position, but it hasn’t been tested at scale by regulators yet. Financial institutions with existing BSA/AML obligations who are considering deploying agent payment infrastructure need to get clear answers from compliance counsel before going live — not after a regulator raises a question.

Sanctions Screening at Agent Speed

OFAC sanctions screening is a standard requirement for financial institutions transacting in US dollars. For human-initiated transactions, screening a counterparty before transaction execution is straightforward — there’s a human in the loop who can pause while the check runs. For an autonomous agent executing high-frequency transactions at machine speed, real-time sanctions screening needs to be embedded at the wallet infrastructure level, not as an afterthought in application code.

Coinbase says it incorporates screening on agentic wallets, and programmable allowlists of counterparty addresses provide a structural control. But the granularity and coverage of that screening — particularly for complex DeFi interactions where funds flow through multiple smart contracts before reaching their destination — is a live risk management question that hasn’t been fully answered publicly.

Unauthorized Overspending and Agent Drift

Programmable spending limits are necessary but not sufficient. A limit of $100 per day prevents catastrophic loss on a single runaway agent, but it doesn’t prevent a systematically misconfigured agent from spending its full daily limit on unintended transactions every single day. The combination of spending limits, counterparty allowlists, and transaction-purpose logging is the minimum viable control set — but organizations need to think carefully about how they’ll detect and respond to agent behavior that’s “within limits” but wrong in direction.

Agent observability — real-time visibility into what each agent is doing, what it’s paying for, and whether that aligns with its intended purpose — is not a feature that comes out of the box. It requires deliberate instrumentation, and for financial applications, it should be treated with the same rigor as any financial system audit capability.

Smart Contract Risk

For agents interacting with DeFi protocols, smart contract risk is a distinct category from operational risk. A bug in a DeFi protocol’s smart contract can result in loss of funds with no recourse — there’s no FDIC insurance, no chargebacks, no dispute resolution mechanism. Enterprises considering DeFi integration through AgentKit need explicit policies on approved protocols, smart contract audit requirements, and maximum exposure limits per protocol — again, independent of spending limit policies that only address the amount spent, not where it’s spent.

What Enterprise Finance and Engineering Teams Should Actually Do Right Now

Given everything above — the genuine capability, the real limitations, and the open compliance questions — what’s the actionable path forward for organizations evaluating Coinbase for Agents in 2026?

Start with a Contained, Observable Use Case

The highest-confidence first deployment is one where: the agent’s financial scope is small and well-defined; the counterparties it transacts with are pre-approved and limited; the transaction volume is low enough to monitor manually at first; and the value at stake from a mistake is below a threshold that would be materially damaging. Pay-per-API-call for a single internal research pipeline, or automated micropayments for a developer tooling workflow, fit this profile well.

Starting with autonomous treasury management or open-ended trading agents is not the right initial move, regardless of how compelling the use case appears on paper. The compliance groundwork, the monitoring infrastructure, and the organizational understanding of how agent financial behavior works all need to be established before scale.

Build Observability Before You Build Features

Before any agent wallet goes live with real funds, the organization needs the ability to see every transaction that agent executes in near-real-time, with enough context to understand why the transaction happened and whether it aligned with the agent’s intended purpose. Onchain records provide an audit trail, but they don’t provide intent context — that has to be logged at the application layer and linked to the transaction IDs.

This is non-negotiable for financial applications. The regulator who asks “why did your agent pay this counterparty on this date?” needs to get an answer, and “the AI decided to” is not a compliant response.

Engage Compliance Counsel on the Identity Question

The identity gap in x402 and agent wallet transactions is the most significant open regulatory question in this space. Organizations operating in regulated industries — banking, lending, insurance, securities — need to get clear legal guidance on how autonomous agent transactions interact with their existing BSA/AML obligations before deploying at any meaningful scale. The answer may be “you need to layer additional screening on top of what the infrastructure provides” or “you need to ensure the human principal’s identity is verifiably associated with each agent wallet.” Get that guidance in writing, then build accordingly.

Use Programmable Policies as a First-Line Control, Not a Last Resort

Spending limits, counterparty allowlists, and time-based transaction caps should be configured before any agent wallet is funded, not added reactively after an incident. Treat the programmable policy layer as a first-class engineering deliverable with its own review and approval process — not as a setting to configure quickly before launch.

Track the Regulatory Direction

The regulatory environment for autonomous agent payments is in genuine flux in 2026. The CFTC has issued guidance on AI in derivatives markets. The OCC has published letters on crypto asset activities in national banks. The EU’s Markets in Crypto Assets Regulation (MiCA) creates a distinct compliance surface for European deployments. None of these frameworks fully address autonomous agent payments yet — they’re all evolving to catch up with the technology. Organizations need a process for tracking this evolution and updating their internal policies when the external requirements crystallize.

The Bigger Picture: What This Means for Fintech Architecture in 2026 and Beyond

Coinbase for Agents is not arriving in isolation. It’s part of a broader structural shift in how software systems relate to financial infrastructure — one that will take years to fully settle but whose direction is now clear enough to plan around.

The Agentic AI Market Trajectory

The agentic AI market was valued at approximately $5.25 billion in 2024 and is projected to reach $199 billion by 2034 at a compound annual growth rate of roughly 36%. McKinsey has projected $3–5 trillion in global agentic commerce volume by 2030. Even discounted heavily for typical market projection optimism, the trajectory suggests that the financial infrastructure supporting autonomous agents is going to become a substantial category — not a niche.

The question for organizations isn’t whether agentic payments will become significant, but whether their financial infrastructure will be positioned to support them when they need to. Building familiarity now, with small and contained use cases, is substantially cheaper than trying to retrofit agentic payment capabilities into systems designed entirely around human-initiated transactions after the market has moved.

The New Financial User Type

Perhaps the most useful mental model for understanding what Coinbase for Agents actually changes is this: financial infrastructure has historically had two user types — consumers and businesses. Both are human legal entities. Coinbase for Agents introduces a third user type: the software agent, which is not a human, not a business in the traditional legal sense, but is nonetheless initiating and completing financial transactions at scale.

That new user type requires new infrastructure (programmable wallets, agent-native payment protocols), new compliance frameworks (accountability models for non-human actors, real-time screening at machine speed), and new governance thinking (how organizations maintain meaningful oversight of agents that may be executing thousands of transactions per day). None of that is fully built yet. But Coinbase for Agents is the first serious attempt to lay the rails.

Who Builds the Guardrails?

The important question that 2026 leaves partially unanswered is: who is responsible for the governance layer that sits between raw agent capability and responsible financial operation? Coinbase provides the infrastructure; the programmable policy layer offers some controls. But the organizational governance, the compliance workflows, the incident response playbooks for runaway agents, and the regulatory engagement — those responsibilities fall squarely on the organizations deploying the technology.

This is identical to the dynamic that played out with cloud infrastructure a decade ago. AWS could offer security groups and IAM roles, but organizations that got breached because they misconfigured those controls couldn’t point to Amazon as the responsible party. The same principle will apply here. Infrastructure providers are building the rails. Operators are responsible for what runs on them.

Conclusion: The Machine as Financial Principal

Coinbase for Agents — AgentKit, x402, Agentic Wallets, and the broader CDP stack — represents a coherent answer to a question that fintech has been quietly circling for years: when AI agents become capable of executing complex, multi-step tasks autonomously, how do they handle the parts of those tasks that require money to change hands?

The answer Coinbase has built is not a graft of crypto capability onto existing financial infrastructure. It’s a purpose-built financial stack for non-human actors — one that treats programmability, speed, auditability, and minimal human dependency as first-order design requirements rather than features to add later.

The x402 protocol’s 75.41 million transactions in 30 days suggest this isn’t a paper architecture. The Blocklords deployment at 50 million-plus onchain transactions demonstrates that agent wallet infrastructure works under real load. The FereAI case study shows autonomous trading and research agents operating productively within defined parameters. The momentum is real.

But the compliance questions are equally real, and they haven’t been resolved by the technology. The accountability gap for autonomous agent transactions, the sanctions screening requirements at machine speed, the smart contract risk in DeFi integrations, and the regulatory frameworks that are still playing catch-up — these are not edge cases to be handled later. They are the conditions of responsible deployment, and organizations that skip this work will encounter it in a less comfortable context.

The machine is now a customer. The infrastructure for that reality is being built faster than the governance frameworks that need to surround it. The organizations that get this right in 2026 will have a meaningful advantage when the governance catches up — because they’ll have already built the habits, the observability, and the risk management discipline that compliant deployment requires.

The non-human customer has arrived. The question is whether your financial infrastructure is ready to serve it responsibly.

Key Takeaways for Practitioners

- Coinbase for Agents (CDP AgentKit + x402 + Agentic Wallets) creates a full financial stack for AI agents as first-class financial principals — not just as interfaces for human accounts.

- x402 has already processed 75.41M transactions in a 30-day window, confirming real production momentum beyond developer experiments.

- USDC on Base provides the settlement layer: ~2-second finality, sub-cent fees, and price stability without the volatility of unpegged crypto assets.

- The compliance accountability gap — who is legally responsible when an autonomous agent transacts? — is the most important unresolved question for enterprise deployment in 2026.

- Traditional fintech APIs and Coinbase for Agents are complementary, not competing: fiat rails remain appropriate for most consumer and institutional fiat flows; agent-native rails handle the autonomous, crypto-settled portion of the stack.

- Start with a contained, observable use case with pre-approved counterparties and low financial exposure before moving to treasury automation or open-ended trading agents.

- Build observability infrastructure before building features — every agent transaction needs enough logged context to reconstruct why it happened.

Leave a Reply